|

|

|

| SW Aviator Magazine is available in print free at FBOs and aviation-related businesses throughout the Southwest or by subscription. |

|

|

|

|

|

|

|

The web's most comprehensive database of Southwest area aviation events.

|

|

|

|

|

|

|

Featured Site:

|

|

|

|

|

A continuosly changing collection of links to our favorite aviation related web sites.

|

|

|

|

|

|

|

|

|

TAX TIME

|

|

Strategies for Aircraft Used in Business

|

By Wendy Simeur and Sharon Gregg, CPA

I can hear your groans from here. Here come big, complicated tax words. Don’t I pay my accountant to know these things? Well, consider this a gentle reminder for your busy, earthbound accountant. In the last few years, special depreciation tax laws have changed significantly for aircraft and other types of equipment purchased for use in business. This article is tailored to help the flying community take advantage of powerful, tax saving strategies. Some of them could result in your writing off over three-quarters of the cost of your airplane in the year of purchase!

Tax laws have been the subject of much scrutiny in recent years, and major tax laws changes were enacted by Congress during the administrations of Presidents Ronald Reagan, Bill Clinton, and George W. Bush. The resulting mixture is a complex interplay of multiple provisions that allow choices, or elections, by the taxpayer. While true that for tax year 2004 a large portion of an airplane used for business may be deducted in the year of purchase, it may not be the most advantageous use of the tax benefit if you do not have sufficient income to absorb the larger deduction. Therefore, we will also explore the more traditional depreciation method.

As you probably know, aircraft owners who fly their aircraft in the course of business are entitled to depreciate the cost of the airplane on the business’ tax return. This is especially beneficial to sole proprietors, partners in partnerships, and shareholders of S corporations. Depreciation is not available for use on aircraft used solely for personal, non-business use.

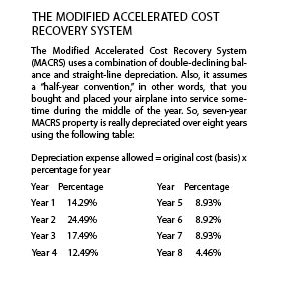

So what is depreciation? Simply put, depreciation is an allowance for wear and tear on fixed assets. Assets with a useful life of more than one year carry a requirement that the cost of the asset be allocated, or prorated, in some fashion over the entire useful life. These assets (called variously long-term assets, fixed assets, or capital assets) produce income over an extended period of time, therefore the cost of acquiring the assets (the accounting principle of matching expenses to revenues) is also spread over a period of time following that. The current method of computing depreciation is the modified accelerated cost recovery system (MACRS), which assigns a life span to different kinds of equipment. Airplanes are assigned a life span of seven years. This means that you can deduct the cost of your airplane over seven years. You report this prorated cost deduction on your company’s tax return as a business expense called “depreciation expense,” otherwise known simply as depreciation. Depreciation offsets income produced by your business, and results in a lower tax bill.

Under normal circumstances, the MACRS system only allows you to take 14.29% of the cost of your airplane as an expense in the year of purchase (see sidebar). However, if you bought an airplane in 2004 (or are planning to buy an airplane sometime before 2007), you have more options than just plain old MACRS. Two types of special depreciation can be used so your business can deduct a higher percentage of the cost of the airplane in the year of purchase.

The first type of special depreciation is called the “Section 179 Election to Expense.” The section 179 election allows you to completely deduct (expense) the cost of your airplane in the year of purchase, up to $102,000 for 2004. (NOTE - If your airplane cost more than $410,000, the expense amount is reduced. If your airplane cost more than $512,000, you cannot use the section 179 election.) To qualify, the airplane must be used more than 50% for business use. It can be new or used property.

The second type of special depreciation is called the “Section 168(k) Special Allowance.” This rule allows you to deduct either 50% or 30% (your choice, but not both) of the cost of the aircraft in the first year of ownership. This deduction can be taken even after the Section 179 election has been used. The special allowance under section 168(k) is for new property only, and it expires after 2004.

Taking advantage of these various provisions represents a timing decision you – with your accountant – must make. The two special provisions under section 179 or section 168(k) allow you to take more in the year of purchase, meaning of course, less in future years.

When taking depreciation on your airplane, you have to keep track of how much you have claimed as depreciation expense on your taxes over the years, and how much of the original purchase price has yet to be written off. The original price you pay for your airplane is called your “basis” in the airplane. Every time you claim depreciation, no matter what type, the amount claimed is subtracted from the original basis, resulting in a smaller adjusted basis. Eventually, after all depreciation expense has been claimed, your adjusted basis in the airplane will be zero.

Here are some examples of how special depreciation can be taken:

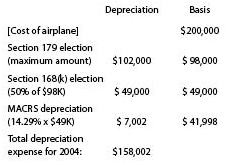

MAXIMUM DEPRECIATION EXPENSE:

Say for example in 2004 you purchased a 1999 Mooney M20 Eagle for $200,000 for use in your business. To claim the maximum deduction on your 2004 business tax return, take the deductions in the following order:

|

|

| By taking advantage of both special depreciation rules in addition to the regular MACRS depreciation deduction, the maximum depreciation allowable on a $200,000 airplane is $158,002 for 2004. For subsequent tax years, the MACRS depreciation percentage will be calculated as if you had purchased the aircraft for $49,000.

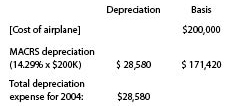

MINIMUM DEPRECIATION EXPENSE:

Obviously, you do not have to use the special depreciation rules if you don’t want to! If you want to minimize your depreciation expense, just use the MACRS depreciation rules:

|

|

|

| For subsequent tax years, the MACRS depreciation percentage will be calculated on the original purchase price of $200,000. |

| |

So, using various combinations of section 179, section 168(k), and MACRS depreciation, for a $200,000 airplane purchased in 2004 you can choose a depreciation expense anywhere between $28,580 and $158,002. If your business has a high taxable income, you may want to take the highest depreciation expense available to reduce your taxable income, and therefore reduce your taxes.

Another consideration when planning your depreciation strategy is how long you intend to keep the airplane. When you sell your airplane, you will have to report the sale on your tax return, and recognize a capital gain on any amount received in excess of your current basis in the airplane. Returning to our two examples above, if the owner in example one sold the airplane for $250,000 in 2005, he or she would have a capital gain of $208,002 ($250,000 - $41,998). Owner two would only have a capital gain of $78,580 ($250,000 - $171,420). So, if you plan on keeping your plane for a very short time, it may not be to your advantage to use the special depreciation rules. However, if you plan to keep your airplane for a longer period, your basis in the airplane will be about the same no matter which depreciation method you choose, and you should base your decision on the tax benefit you would receive from a high depreciation expense in 2004.

So now you’re wondering, what qualifies my aircraft as a business expense? Or, how do I start a business to take advantage of these special rules? Those questions are beyond the scope of this article and best left to the advice of your personal accountant and attorney. Always have a tax professional review business purchases for tax ramifications. All tax advice is worth what you paid for it, and in this case the advice was free.

Hopefully the information contained here helps you with your business tax strategy. The special depreciation rules were created and updated in the aftermath of the September 11 attacks to stimulate the economy by encouraging the purchase of equipment by businesses. So make sure you are receiving all the benefits you can for your own business! Talk to your accountant today.

Wendy Simeur is the Chief Financial Officer for Momentum Interactive Aviation, a company that specializes in instructor support, and interactive flight training & planning software, including a new weight and balance program. You can see the software or contact Wendy at Momentum-i.com.

Sharon Gregg is a practicing CPA in Albuquerque, NM. Prior to opening her accounting firm she was a Revenue Agent for the IRS. YShe prepares income tax returns for all types of businesses, including corporations, limited liability companies, partnerships, and sole proprieterships. You can contact Sharon at 505-296-7400.

|

Wendy Simeur is the Chief Financial Officer for Momentum Interactive Aviation, a company that specializes in instructor support, and interactive flight training & planning software, including a new weight and balance program. You can see the software or contact Wendy at Momentum-i.com.

|

Click here to return to the beginning of this article. |

|